Three Regulators, One Market

The short version

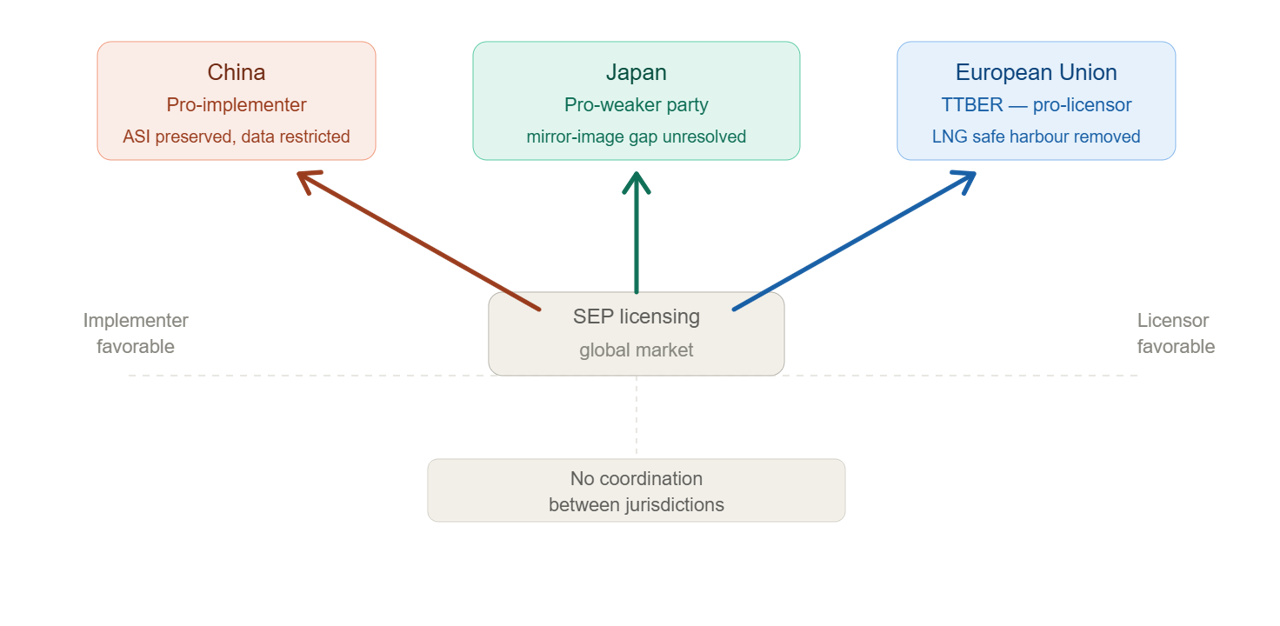

The EU, Japan, and China have each issued significant IP licensing instruments within the past six weeks, acting in parallel but without coordination.

Their vectors point in different directions: the revised EU Technology Transfer Block Exemption Regulation tilts toward licensor protection by eliminating the Licensing Negotiation Group safe harbor; Japan’s new draft guidelines target dominant-buyer extraction of IP and know-how from weaker suppliers; China’s post-DS611 architecture preserves anti-suit injunction capability while restricting the outbound transfer of data relevant to foreign licensing proceedings.

Japan’s instrument contains an analytical gap worth naming directly: the same statutory framework that prohibits dominant buyers from extracting IP from smaller suppliers should, in principle, equally prohibit dominant implementers from engaging in holdout against smaller SEP licensors. The JFTC has not addressed that symmetry, and it should.

For SEP practitioners and licensors, the integrated picture is neither uniformly favorable nor uniformly hostile. It is multi-polar. Strategy built around any single jurisdiction’s posture is increasingly incomplete.

I. Why this moment matters

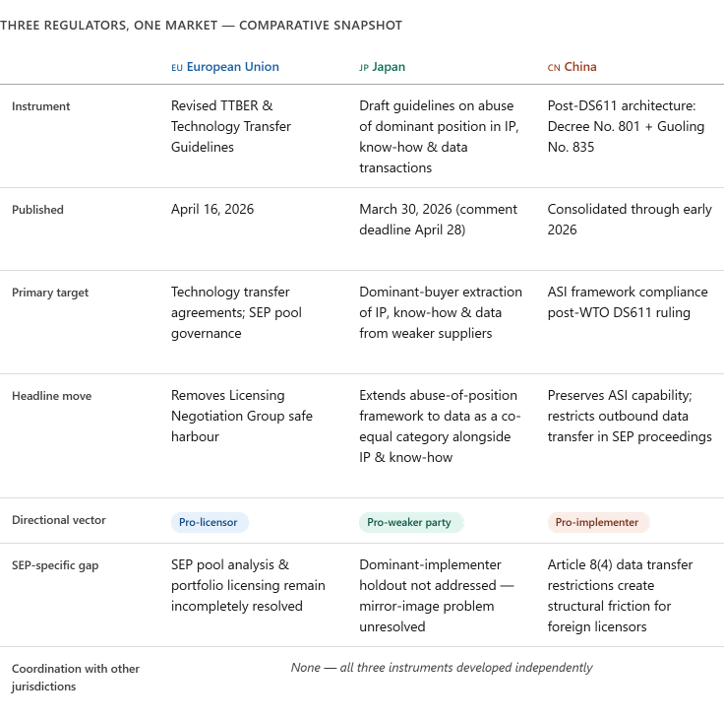

Something significant happened between mid-March and late April 2026 that has received no coordinated attention: three of the world’s most consequential IP licensing jurisdictions each published major regulatory instruments affecting the environment in which SEP licensing negotiations occur. The European Commission issued its revised TTBER and Technology Transfer Guidelines on April 16. Japan’s JFTC, SMEA, and JPO jointly published draft guidelines on abuse of dominant position in IP, know-how, and data transactions on March 30. And China’s post-WTO DS611 regulatory architecture (covered in detail in April: “China Didn’t Retreat on SEPs. It Changed the Rules of the Game.” and “China’s Regulatory Upgrade: The Threat Nobody Is Talking About”) has continued to consolidate through implementation of State Council Decree No. 801 and Guoling No. 835.

None of these instruments was designed with the others in mind. They emerged from different domestic policy processes, different institutional cultures, and different industrial constituencies. But they are landing simultaneously on the same multinational licensors and implementers, and their combined effect is something more complex and more consequential than any individual instrument suggests.

II. The EU: a genuine pro-licensor signal

I covered the TTBER in detail when it published in April (“The EU’s New Tech Transfer Guidelines”), so I will not re-argue it here. The headline for SEP licensors was the removal of the Licensing Negotiation Group safe harbor. LNGs (collective implementer negotiation groups) had enjoyed safe harbor treatment under the prior framework on the theory that they helped balance licensor bargaining power. The revised regulation eliminates that protection. The Commission’s reasoning, which I find correct, is that LNGs in practice function as coordinated holdout mechanisms rather than efficiency-promoting structures. Removing the safe harbor is an acknowledgment that implementer coordination is a real competition problem, not a theoretical one.

That is a meaningful pro-licensor move. The revised TTBER and guidelines still leave important questions unresolved, particularly around SEP pool analysis and the treatment of portfolio licensing. But the directional signal is clear, and it matters because the EU is, for now, still the jurisdiction in which the foundational FRAND precedents were established and in which the most technically sophisticated SEP litigation occurs.

III. Japan: the mirror-image problem

Japan’s March 30 draft instrument is less visible outside Japanese practitioner circles, and its connection to SEP licensing is indirect. It deserves more attention than it has received.

The backstory: the JFTC has been building toward this instrument since a major 2019 fact-finding survey documented systematic extraction of patents, know-how, and technical data from smaller Japanese manufacturing suppliers by dominant buyers (large OEMs and system integrators who leveraged purchasing relationships to obtain IP at below-market or zero compensation). A new “IP Transaction Normalization Working Group,” chaired by attorney Izumi Hayashi of Sakurazaka Law Office, ran from August 2025 through March 2026, producing a report that the draft guidelines directly implement. The joint JFTC/SMEA/JPO instrument addresses abuse of superior bargaining position in transactions involving IP rights, know-how, and data (a meaningful new addition to the prior framework’s scope).

The target is the dominant buyer who coerces a weaker supplier into disclosing trade secrets without fair compensation, assigning patents as a condition of continued business, tolerating unilateral IP ownership terms in joint development contracts, or providing manufacturing process data without adequate consideration. Those are genuine, well-documented problems in Japanese supply chains, and the instrument is a serious response to them.

The statute that governs this conduct, however, is Article 2(9)(5) of the Antimonopoly Act, which prohibits abuse of superior bargaining position. It is not directionally limited. It applies wherever one party holds superior bargaining position over another and exploits it to impose unjust disadvantage. The draft guidelines address only one polarity of that relationship.

The mirror scenario is analytically identical. A dominant implementer (a major automotive OEM, a large consumer electronics platform, a global device manufacturer) who refuses to engage in good-faith SEP licensing negotiations with a smaller licensor is exploiting superior bargaining position to impose unjust disadvantage on a party who cannot easily walk away. The licensor who has made a FRAND commitment cannot simply refuse to deal. The implementer who knows that knows it. Sustained holdout by a dominant implementer is, under the same framework the JFTC is now developing, structurally indistinguishable from the extraction conduct the guidelines are designed to prevent.

The JFTC’s existing IP Guidelines, last amended in 2016, do address SEP-specific issues including injunctions and refusal to license. But they operate within an exclusionary-conduct framework, not the relational abuse-of-position framework that the new instrument develops. That is a different analytical register, and the gap between them is real. The March 2026 draft does not bridge it.

This matters practically, not just analytically. Japan’s automotive and IoT sectors (among the primary battlegrounds for next-generation SEP licensing in 5G and 6G applications) are precisely where dominant-implementer holdout dynamics are most pronounced. Many Japanese component suppliers hold declared SEPs. Many of their largest customers are the same OEMs whose supply-chain IP practices the new guidelines are designed to constrain. The JFTC has, in effect, developed a sophisticated analytical framework for one side of that relationship. The question it has not answered is whether that framework applies symmetrically.

I do not think the JFTC made a deliberate decision to exclude SEP licensing relationships from the instrument’s scope. The more likely explanation is that the Working Group’s mandate was framed around supply-chain normalization, and SEP licensing simply was not in view. But the logical implication of the instrument, read carefully, is that dominant-implementer holdout should be as analytically suspect as dominant-buyer IP extraction. The JFTC should say so explicitly in the final version of the guidelines.

The public comment window for the March 30 draft closed today, April 28. I assessed whether to file a formal comment, but the submission requirement is Japanese-language only and the timeline (48 hours after I became aware of the instrument) made a properly drafted submission impractical. This article is what I would have submitted. There will be a final instrument, likely later in 2026, and that will be the right moment to press this argument on the record. I intend to do so.

IV. China: recalibration, not retreat

My April coverage traced China’s post-DS611 regulatory architecture in detail (“China Didn’t Retreat on SEPs. It Changed the Rules of the Game.” and “China’s Regulatory Upgrade: The Threat Nobody Is Talking About”), and I will not reconstruct the full argument here. The short version is that China adjusted its formal procedural posture in ways minimally sufficient to address the WTO dispute panel’s findings while preserving the substantive tools (ASI capability, domestic jurisdiction preference, data transfer restrictions) that make Chinese proceedings operationally significant in global SEP licensing strategy.

The provision I continue to watch most closely is Article 8(4) of the DS611 implementing rules, which restricts the outbound transfer of certain data and evidence in the context of SEP licensing disputes. A licensor building a global evidentiary record for a FRAND rate determination (the kind of proceeding that requires comparable license data, technical contribution analysis, and portfolio valuation) faces structural friction when the relevant commercial and technical data sits with Chinese implementers or in Chinese corporate systems. That friction is not incidental. It is a designed feature of a regulatory architecture whose overall orientation is implementer-favorable.

V. The integrated picture

A licensor operating across all three jurisdictions simultaneously now faces this environment: a European framework that has signaled genuine support for licensor interests by removing LNG protection, but that still leaves SEP pool treatment and portfolio licensing questions incompletely resolved; a Japanese framework that has developed sophisticated tools for addressing IP exploitation in vertical relationships, but that has not yet applied those tools symmetrically to SEP holdout dynamics; and a Chinese framework that presents a compliant face to WTO scrutiny while preserving the architecture that makes domestic proceedings attractive to implementers.

The net effect is not uniformly favorable or hostile. It is multi-polar. And the absence of any coordination mechanism among these three frameworks means that jurisdictional arbitrage (by both licensors and implementers) will continue to drive where disputes are initiated and where they resolve.

That dynamic will not improve on its own. The instruments themselves are not moving toward convergence. The standards community, and specifically those practitioners and organizations with the standing to engage each of these frameworks at the regulatory level, should be doing so actively, in all three jurisdictions, simultaneously. Engaging one at a time is no longer adequate.

Jim Harlan is an independent intellectual property practitioner with approximately 25 years of experience in SEPs, FRAND licensing, and standards policy. Standards at Risk covers patent licensing, global standards policy, and innovation market dynamics. Subscribe at standardsatrisk.substack.com.